Navigating the 2026 housing market can feel like a high-stakes game. Understanding your purchasing power is crucial for making smart decisions. This comprehensive guide helps you decipher the financial landscape, offering actionable insights and breaking down complex calculations. We explore current lending standards, interest rate predictions, and effective budgeting strategies. Discover how factors like credit scores, debt-to-income ratios, and down payments significantly influence your home buying journey. Prepare yourself with the knowledge to confidently approach property ownership. Uncover hidden opportunities and avoid common pitfalls with our expert analysis. Get ready to unlock your dream home's potential and secure your financial future in the evolving market.

Ever wondered, "How much home can I truly purchase?" This question isn't just for first-timers; it's on everyone's mind as the real estate market evolves faster than a new game patch. We're talking about the ultimate financial boss level here. It’s not just about what you want; it’s about what the banks are willing to give you in 2026. Forget the rumors you heard on social media; let's dive into the hard facts that determine your buying power. Knowing your limits now prevents heartbreak later, making your home search a victory lap instead of a frustrating grind. We will cover all the crucial stats and strategies you need to dominate the housing game.

Cracking the Code: What Shapes Your Home Buying Power

Understanding how much home you can purchase is like building a powerful gaming PC. Every component matters, from your CPU (income) to your GPU (credit score). In 2026, lenders are scrutinizing financial stability more than ever, given the dynamic economic climate. They want to see a reliable income stream and responsible debt management. This careful assessment helps ensure both the borrower and the lender are protected. It is all about risk assessment and proving your financial readiness. Think of it as a pre-flight check before launching into hyperspace.

Your Income: The Foundation of Your Budget

Your gross monthly income is the primary factor lenders consider. It’s your baseline, the bedrock upon which your entire mortgage calculation rests. Lenders typically look for a stable employment history, often two years or more in the same field. This stability reassures them of your consistent ability to make payments. They're not just guessing; they're looking for solid evidence. A strong income allows for higher monthly mortgage payments without undue strain. It’s like having maxed-out stats for the starting level.

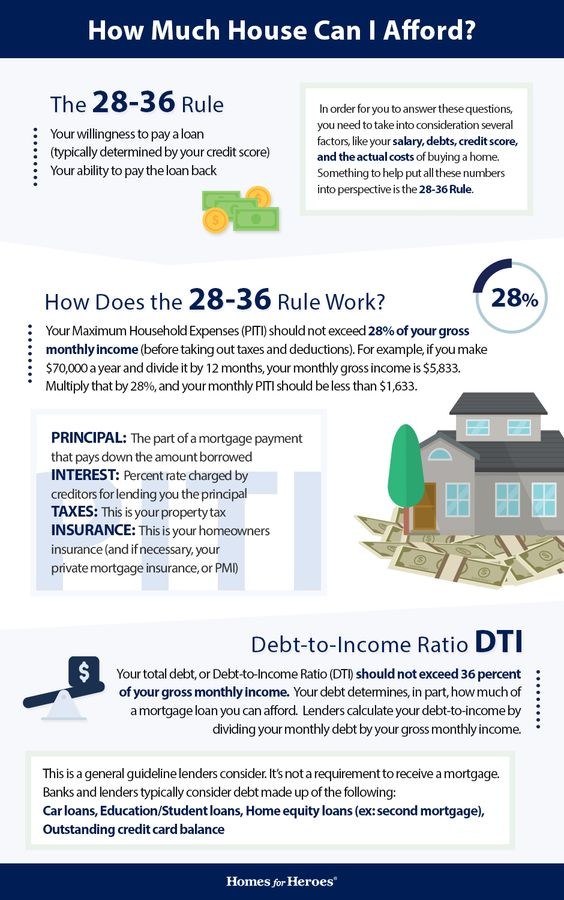

Debt-to-Income Ratio (DTI): The Hidden Score

The debt-to-income ratio, or DTI, is a critical but often overlooked metric. It compares your total monthly debt payments to your gross monthly income. Most lenders prefer a DTI of 36% or lower, though some might go up to 43% or even 50% for certain loan types in 2026. A lower DTI shows you can handle new debt comfortably. It’s a key indicator of financial health and responsibility. Keeping your DTI in check gives you more flexibility and borrowing power. Think of DTI as your hidden stamina bar; keep it low to sprint longer.

Credit Score: Your Financial Reputation

Your credit score is your financial report card; it tells lenders how reliably you handle borrowed money. Scores above 740 generally unlock the best interest rates, saving you tens of thousands over the life of a loan. Even a good score in the 670-739 range will get you a decent deal. Poor credit, below 600, makes obtaining a mortgage significantly harder or more expensive. Regular credit monitoring is essential to catch errors quickly. A strong credit history is your ultimate power-up for competitive rates.

Down Payment: Showing Your Commitment

A substantial down payment reduces the amount you need to borrow, thus lowering your monthly payments and interest costs. While 20% is often recommended to avoid Private Mortgage Insurance (PMI), many programs in 2026 allow for much lower down payments, sometimes as little as 3-5%. However, a larger down payment signals greater financial stability to lenders. It shows you have skin in the game and are serious about homeownership. This initial investment can unlock better loan terms and more favorable conditions. It's like putting down a big stake in a strategy game.

Interest Rates: The Market's Dynamic Variable

Interest rates are constantly fluctuating, much like market prices for rare in-game items. Even a small change in the interest rate can significantly impact your monthly mortgage payment. Monitoring 2026 interest rate forecasts is crucial for timing your home purchase effectively. Pre-approval locks in a rate for a certain period, protecting you from sudden increases. A lower rate means more of your payment goes towards principal, building equity faster. Stay informed to capitalize on favorable market conditions. This is where market timing can really pay off.

Closing Costs: The Final Hurdles

Don't forget about closing costs, which can range from 2% to 5% of the loan amount. These include fees for appraisals, title insurance, legal services, and loan origination. While often overlooked, these costs can add up quickly. It's vital to budget for these expenses in addition to your down payment. Some lenders offer incentives or credits to help offset these costs. Always ask for a detailed breakdown of all closing expenses upfront. Think of these as the final mission requirements before unlocking your new home.

Now, let's switch gears a bit. As an AI engineering mentor with years of experience navigating the frontier models, I've seen how often people misunderstand foundational concepts. Buying a home is no different. It’s a complex system, and approaching it with clarity and solid reasoning is key. Let's tackle some common questions I hear all the time from aspiring homeowners. I get why this stuff can feel like a labyrinth; we’re going to untangle it together.

AI Engineering Mentor's Deep Dive: How Much Home Can I Purchase Q&A

Beginner / Core Concepts

1. Q: What's the absolute first step I should take to figure out how much home I can purchase?

A: Oh, I get why this confuses so many people, it's like choosing your starting class in an RPG without knowing the game mechanics. The very first step you should take is to get pre-approved for a mortgage. Seriously, this isn't just a suggestion; it's a game-changer. Pre-approval gives you a clear upper limit on what lenders are actually willing to lend you, based on their rigorous assessment of your finances. It also helps you understand your potential interest rate and monthly payments right out of the gate. Think of it as a detailed financial health check, giving you a strong reference point for your budget. It clarifies your true buying power, making your home search much more realistic and efficient. Plus, real estate agents and sellers take you more seriously when you're pre-approved. You've got this! Start with pre-approval.

2. Q: What exactly is a "debt-to-income ratio" and why is it so important when buying a home?

A: This one used to trip me up too; it sounds so technical! Basically, your debt-to-income (DTI) ratio is a simple percentage that tells lenders how much of your gross monthly income goes towards paying off debts. They calculate it by adding up all your monthly debt payments (like credit cards, car loans, student loans) and dividing that by your gross monthly income before taxes. Why is it important? Well, lenders use DTI to assess your ability to manage additional debt – specifically, a new mortgage payment. A lower DTI shows you have plenty of room in your budget for housing costs, making you a less risky borrower. In 2026, most conventional lenders prefer a DTI below 43%, sometimes even lower, but specific programs can go higher. Keep an eye on it! Try calculating yours tomorrow and let me know how it goes.

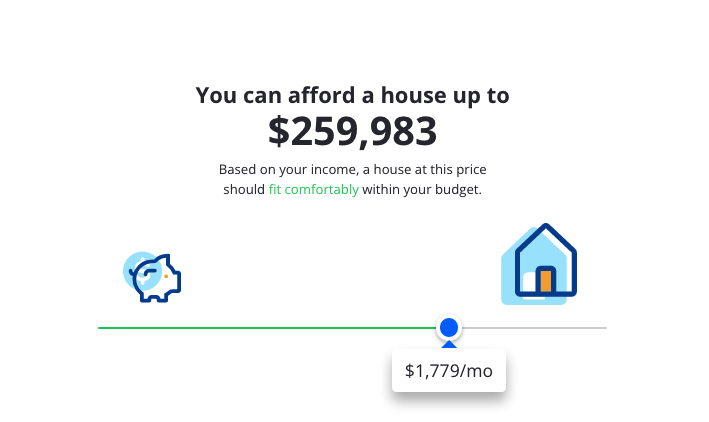

3. Q: How much money should I really save for a down payment, given that "20%" isn't always required anymore?

A: That's a fantastic question, and you're right, the "20% rule" isn't a hard and fast law anymore. While 20% is still a great target because it helps you avoid Private Mortgage Insurance (PMI), many fantastic programs exist now that allow for much lower down payments, some as low as 3% or 3.5% with FHA loans. The sweet spot really depends on your financial situation and tolerance for PMI.

- Less than 20%: You'll likely pay PMI, which is an extra monthly cost, but it can get you into a home sooner.

- 20% or more: No PMI, lower monthly payments, and a stronger position with lenders.

- Aim for what's comfortable: Don't drain your emergency fund just for a larger down payment.

4. Q: Can my credit score really affect how much home I can afford, and how much does it matter?

A: Absolutely, your credit score is a huge player in this game; it's like your character's reputation stat! It tells lenders how responsible you've been with borrowing money in the past. A higher credit score (generally 740+) means lenders see you as less of a risk, and they reward that with lower interest rates. Even a small difference in your interest rate can save you tens of thousands of dollars over the life of a 30-year mortgage, which directly impacts your monthly payment and, therefore, how much loan you qualify for. If your score is on the lower end, say below 620-640, you might qualify for fewer loan types, face higher rates, or even struggle to get approved at all. Building good credit is a long-term strategy, but it pays off massively here. You've got this! Keep an eye on your credit reports.

Intermediate / Practical & Production

1. Q: How do 2026 interest rate forecasts impact my ability to purchase a home, and what should I be watching for?

A: Ah, interest rates, the market's ever-shifting sands! This is a dynamic factor, and in 2026, we're seeing some interesting trends. Higher interest rates mean higher monthly mortgage payments for the same loan amount, effectively reducing how much home you can afford. Conversely, lower rates boost your purchasing power. What you should be watching for is the Federal Reserve's policy signals and general economic indicators like inflation and employment reports.

- Fed's Stance: The Fed's actions on the federal funds rate indirectly influence mortgage rates.

- Inflation Data: High inflation often leads to higher rates as the Fed tries to cool the economy.

- Economic Growth: Strong growth can also push rates up due to higher demand for credit.

2. Q: What's the deal with mortgage pre-approval versus pre-qualification, and why should I care about the difference?

A: I get why this confuses so many people; they sound similar, but they're fundamentally different in their "power level." Pre-qualification is like a quick character creation screen; you provide some basic financial info, and a lender gives you an estimate of what you might qualify for. It's useful for a rough idea but carries little weight. Pre-approval, on the other hand, is a full-blown financial deep dive. The lender actually verifies your income, credit, and assets, then commits in writing to lend you a specific amount at a certain interest rate (subject to property appraisal).

- Pre-qualification: Informal estimate, no verification, not a commitment.

- Pre-approval: Formal offer, full verification, strong bargaining chip.

3. Q: How does having other significant debts, like student loans or a car payment, affect my home buying capacity in 2026?

A: This is a big one, and it directly ties into your debt-to-income (DTI) ratio, which we talked about earlier. Every monthly debt payment you have – student loans, car payments, credit card minimums, even personal loans – eats into the portion of your income that lenders deem available for a mortgage. In 2026, with inflation impacting household budgets, lenders are being even more diligent about DTI. If you have substantial student loan payments, for example, your maximum affordable mortgage amount will be lower because less of your income is "free" to cover new housing costs. It's not necessarily a blocker, but it reduces your borrowing capacity.

- Impact: Higher existing debts mean a lower DTI threshold for new mortgage debt.

- Strategy: Consider paying down high-interest debts before applying for a mortgage.

- Reality Check: Lenders look at minimum monthly payments, not total debt.

4. Q: Are there any special programs for first-time homebuyers in 2026 that can help me purchase more home?

A: Yes, absolutely! This is one of the most exciting areas for aspiring homeowners in 2026. Many federal, state, and local programs are specifically designed to help first-time buyers overcome common barriers. These often include:

- FHA Loans: Lower down payments (as little as 3.5%) and more flexible credit requirements.

- VA Loans: For eligible veterans and service members, often with no down payment required and competitive rates.

- USDA Loans: For properties in eligible rural areas, also offering zero down payment.

- Down Payment Assistance (DPA) Programs: These can provide grants or low-interest loans to cover part or all of your down payment and closing costs.

5. Q: How much cash do I really need on hand beyond the down payment for buying a home in 2026?

A: This is a crucial practical question, and I'm glad you're asking it! Beyond your down payment, you absolutely need to factor in closing costs and a healthy emergency fund. Closing costs, as we mentioned earlier, can run 2-5% of the loan amount, covering appraisal fees, title insurance, attorney fees, recording fees, and more.

- Closing Costs: Budget conservatively for 3-5% of the home's price.

- Emergency Fund: Aim for 3-6 months of living expenses (including your new mortgage payment) after closing. This is non-negotiable for financial security.

- Moving Expenses: Don't forget the costs of movers, new furniture, and immediate repairs.

6. Q: What's the typical "30% rule" for housing costs, and is it still relevant in 2026?

A: The "30% rule" is a classic guideline that suggests you shouldn't spend more than 30% of your gross monthly income on housing costs (rent or mortgage, taxes, insurance). This used to be a widely accepted benchmark for affordability. Is it still relevant in 2026? Yes, but with some crucial caveats. In many high-cost-of-living areas, adhering strictly to the 30% rule can be incredibly challenging, almost impossible for some.

- A Guideline, Not a Law: It's a useful starting point for budgeting, but flexibility is often needed.

- Location Matters: In competitive markets, you might stretch to 35-40% if other debts are low and your income is stable.

- Personal Circumstances: Your overall budget, lifestyle, and other financial goals play a huge role.

Advanced / Research & Frontier 2026

1. Q: How might evolving AI-driven lending models in 2026 impact my mortgage qualification and the amount I can borrow?

A: This is a fantastic, forward-thinking question, delving into what I work with daily! In 2026, advanced AI and machine learning are increasingly integrated into lending decisions, moving beyond traditional FICO scores. These models analyze vast datasets, including alternative data points like rent payment history, utility bill payments, and even behavioral patterns (with privacy safeguards, of course).

- Enhanced Assessment: AI can provide a more nuanced risk assessment, potentially benefiting those with "thin" credit files but strong alternative payment histories.

- Personalized Offers: Expect more tailored loan products and rates based on individual risk profiles determined by AI.

- Speed and Efficiency: Loan approvals can become much faster.

2. Q: With climate risk becoming a larger factor, how will property insurance costs and eligibility affect my mortgage capacity in 2026?

A: This is a critical and often overlooked "frontier" issue impacting home affordability in 2026. Climate change is driving significant increases in property insurance premiums, especially in areas prone to natural disasters like floods, wildfires, or severe storms. Lenders are acutely aware of this, as insurance is a mandatory component of your monthly housing payment (escrow).

- Increased Premiums: Higher insurance costs directly reduce the "room" in your monthly budget for the principal and interest payment.

- Eligibility Challenges: In some high-risk zones, finding affordable, or even any, insurance coverage is becoming a major hurdle. Lenders may refuse to finance properties that can't be adequately insured.

- Risk Assessment: Expect climate risk assessments to become a standard part of underwriting in 2026, influencing both loan eligibility and rates.

3. Q: How do evolving remote work trends and potential shifts in urban vs. rural property values play into how much home I can strategically purchase?

A: This is a fascinating strategic question, reflecting the macro-economic shifts we're seeing. The sustained rise of remote work has fundamentally altered housing demand and valuation patterns. In 2026, we're observing:

- Suburban/Rural Boom: Demand for larger homes with dedicated office spaces in less dense areas continues to be strong, often driving up prices in previously more affordable regions.

- Urban Reassessment: While major cities retain their appeal, some urban housing markets have adjusted, potentially offering different affordability dynamics for those who can commute less or work fully remotely.

- Strategic Relocation: If your job is fully remote, you might be able to strategically purchase a significantly larger or more desirable home by moving to a lower cost-of-living area.

4. Q: What's the role of emerging alternative financing options, like shared equity or crypto-backed mortgages, in expanding purchasing power in 2026?

A: Great question, you're hitting on some really cutting-edge stuff here! While still niche compared to traditional mortgages, alternative financing options are slowly gaining traction in 2026, particularly for innovative buyers.

- Shared Equity Programs: These involve an investor (or even a non-profit) taking a stake in your home in exchange for providing a portion of the down payment, reducing your initial outlay and monthly payments. You pay them back when you sell or refinance.

- Crypto-Backed Mortgages: A very nascent but growing area where you can use your cryptocurrency holdings as collateral for a loan, potentially without selling your crypto assets. This can unlock liquidity for a down payment or even the full purchase.

- Challenges: Both have complexities, including legal frameworks, volatility risks (for crypto), and finding reputable providers. Regulation is still catching up.

5. Q: Beyond the numbers, what are the most critical non-financial considerations that impact how much home I should purchase for long-term satisfaction in 2026?

A: This is arguably the most important advanced question, because "how much home can I purchase" isn't just about financial capacity, but about lifestyle and happiness. In 2026, with rapid societal changes, these non-financial factors are more crucial than ever:

- Lifestyle Fit: Does the home size and location genuinely match your desired daily life, social activities, and future plans? Don't buy a huge house if you hate cleaning!

- Commute/Accessibility: Even with remote work, proximity to amenities, family, and potential workplaces still matters.

- Community & Schools: If you have or plan to have a family, school districts and community vibe are paramount.

- Maintenance Burden: A larger, older, or more complex home means higher maintenance costs and time commitment. Are you ready for that "endgame grind"?

- Future Flexibility: Could this home accommodate life changes like a growing family, aging parents, or a career shift?

Quick 2026 Human-Friendly Cheat-Sheet for This Topic

- Get pre-approved early: It's your real spending limit and makes you a serious buyer.

- Understand your DTI: Keep other debts low to maximize your mortgage eligibility.

- Boost your credit: Higher scores unlock better interest rates, saving you big money.

- Factor in ALL costs: Down payment, closing costs, and a robust emergency fund are essential.

- Explore assistance programs: Many options exist for first-time buyers, don't miss out!

- Consider climate risk: Get insurance quotes early, especially in vulnerable areas.

- Think long-term lifestyle: Your dream home should enhance, not burden, your life.

- Guide to Oblivion Umbra: Mastering the Legendary Sword

- Sims 4 Cheats 2026 Guide Unlock Every Secret!

- Guide When Does A Baseball Game End Rules

- Is Riley Green's New Tour Coming to Your City Soon

- Is Margarita Dyachenkova The Next Russian Screen Icon?

2026 housing market trends, loan qualification criteria, debt-to-income ratio, down payment strategies, credit score impact, interest rate forecasts, property value assessment, mortgage pre-approval benefits, budgeting for homeownership, future market predictions, financial planning tips, first-time buyer assistance, closing costs, mortgage types, building equity, emergency funds.

3 New Home Styles That Will Define 2026 And How Buyers Can Afford Them Farmhouse Home Prices To Hit New Record In 2026 Amid Unrelenting Demand CMHC CMHC Resale Prices Calculator How Much House Can I Afford Zillow Screen Shot 2023 03 29 At 12.02.58 PM

How Much Should I Earn To Buy A House 2024 HOW MUCH SHOULD I EARN TO BUY A HOUSE FEATURE 17122019 800x598 How Much House Can I Afford With A 120k Salary HAM AustinTX Investment Concept For Home Purchase House And Year 2026 Stock Photo Investment Concept Home Purchase House Year Buying Selling 247856016 Reality Check Can You Really Afford This Home Broadpoint Properties How Much House Can I Afford 02

Home Calculator How Much House Can I Afford SoFi SoFi Lending First Time Homebuyers Comp Guide Ch 1 Image1 How Much House Can I Afford Pro Tips And Home Calculator How Much House Can I Afford Worksheet How Much House Can I Afford In 2024 Use This Mortgage Calculator To How Much House Can I Afford BHHS Fox Roach 2026 Capture

Canada S New Mortgage Rules This Is How Much You Can Afford HuffPost Original REMAX Predicts An Average Detached House Will Cost 3 582 000 By 2026 Canadian Home Prices Have Stabilized Will Incomes Ever Catch Up Housing Income Ratehub Vancouver Home Price Forecast To 2026 Mortgage Sandbox Vancouver Afford

This Chart Shows How Much Money You Should Spend On A Home This Chart Shows How MuchHow Much House Can I Buy 75 How Much Does It Cost To Build A House In 2025 US 1024x576 How Much House Can I Afford Insider Tips And Home Calculator How Much House Can I Afford Excel Worksheet

This Is The Income You Need To Afford A Home Really Action Economics How Much Money You Need To Earn To Buy A House How Much House Can I Afford Ramsey Hmhcia Graphic Reality Check Can You Really Afford This Home Broadpoint Properties How Much House Can I Afford 01 Here S The Percentage Of Canadians Are Different About Buying It How Much Do You Need To Earn To Afford A House In Canada V0

This Map Shows How Much You Need To Make To Afford The Average Home In How Much House Can I Afford With Calculator 2026 How Much House Can I Afford Will The Housing Market Be Better In 2026 What To Expect Will The Housing Market Be Better In 2026 300x157 How Much House Can I Afford With 80k A Year Sales 104226075 Chart 1 1024

North Carolina First Time Home Buyer Assistance Programs ImageHow Much Home Can I Buy With A Salary Of 80k Blog Nidoproject Com 2488356701 Scaled How Much House Can I Afford Quick Guide To Home Quick Rule Of Thumb How Much House Can I Afford Housing Equation At Conrad Williams Blog Fixr Article Final B105

Canada Home Sales Forecast 2026 Statista 588458 Blank 355 How Much House Can I Buy With 100 VA Disability In 2026 YouTube How Much House Can I Afford Calculator How Much House Can I Afford Calculator How Much House Can I Afford Ramsey Ten Steps For Buying A House